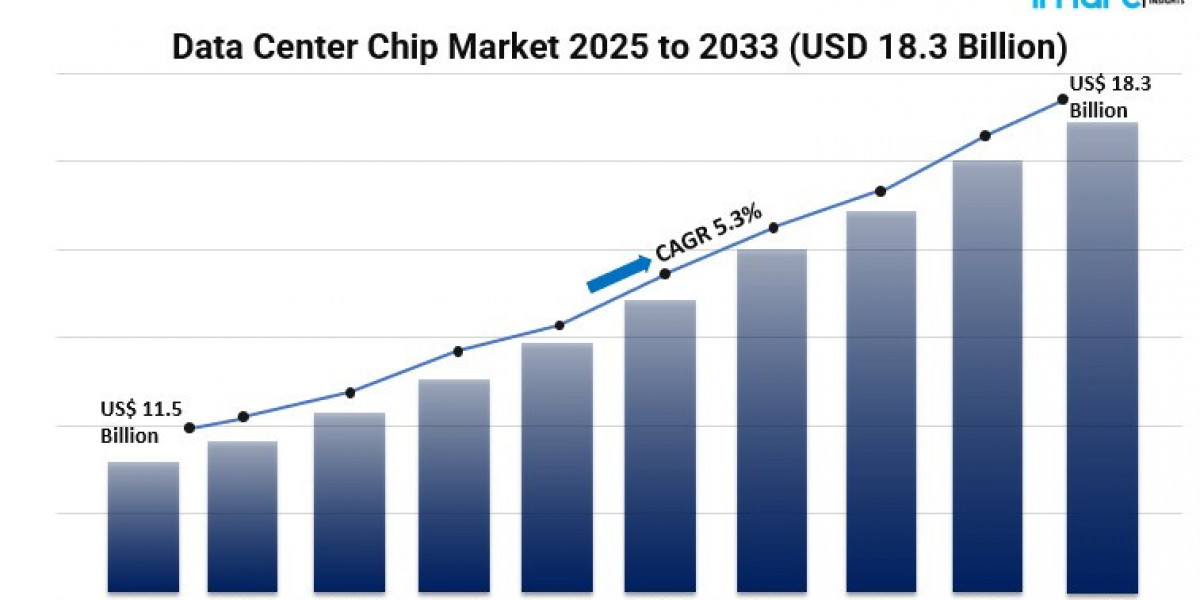

The global data center chip market is experiencing significant growth, driven by the increasing demand for cloud computing, artificial intelligence (AI), and high-performance computing (HPC). In 2024, the market was valued at USD 11.5 billion and is projected to reach USD 18.3 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 5.3% during the forecast period from 2025 to 2033. This expansion is fueled by advancements in semiconductor technology, the proliferation of data-driven applications, and the need for efficient data processing solutions in various industries.

Study Assumption Years

- Base Year: 2024

- Historical Years: 2019–2024

- Forecast Years: 2025–2033

Data Center Chip Market Key Takeaways

- Market Size and Growth: The market was valued at USD 11.5 billion in 2024 and is expected to reach USD 18.3 billion by 2033, growing at a CAGR of 5.3%.

- Dominant Chip Types: Graphics Processing Units (GPUs) lead the market due to their efficiency in handling parallel processing tasks.

- Technological Advancements: The adoption of 5nm semiconductor processes is enhancing chip performance and energy efficiency.

- Industry Applications: Key sectors driving demand include BFSI, IT & Telecom, and cloud service providers.

- Regional Leadership: North America holds the largest market share, attributed to its robust IT infrastructure and technological innovations.

What Are the Key Growth Drivers in the Data Center Chip Market?

Advancements in Semiconductor Technology

The start of new chip making ways, like the 5nm tech, has made data center chips work better and use less power. These new steps let us make stronger chips that can handle tough jobs, helping to meet the rising needs of AI and HPC uses.

Surge in Data Traffic and Cloud Adoption

A big jump in data making and use is pushing the need for data center fixes that can grow and work well. As more firms and people use cloud help, the need for strong data handling is key, making the data center chip market grow.

Integration of AI and Machine Learning Workloads

Putting AI and machine learning into data centers means we need special chips like GPUs and TPUs. These chips are made for many tasks at once, making AI work better and more smooth, and so, making more people want advanced data center chips.

Market Segmentation

By Chip Type

- Graphics Processing Unit (GPU): Dominates the market due to its parallel processing capabilities, essential for AI and HPC applications.

- Application-Specific Integrated Circuit (ASIC): Custom-designed chips optimized for specific tasks, offering high efficiency.

- Central Processing Unit (CPU): Traditional processors handling general-purpose computing tasks.

- Field-Programmable Gate Array (FPGA): Flexible chips that can be programmed to perform specific functions, providing adaptability.

- Others: Includes various specialized chips catering to niche applications.

By Data Center Size

- Small and Medium Size: Data centers catering to regional or smaller-scale operations.

- Large Size: Hyperscale data centers supporting global cloud services and enterprise operations.

By Industry Vertical

- Banking, Financial Services, and Insurance (BFSI): High demand for secure and efficient data processing solutions.

- Manufacturing: Utilization of data analytics and IoT for operational efficiency.

- Government: Implementation of digital services and data management systems.

- Information Technology and Telecom: Infrastructure supporting cloud services and telecommunications.

- Retail: E-commerce platforms requiring robust data processing capabilities.

- Transportation: Integration of data analytics for logistics and operations.

- Energy and Utilities: Data management for smart grids and energy distribution.

- Others: Various sectors adopting data-driven solutions.

Breakup by Region

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Which Region Dominates the Data Center Chip Market?

North America leads the global data center chip market, buoyed by its advanced IT infrastructure, noteworthy investments in cloud computing, and the presence of major tech companies. The increasing focus of the region on technological innovation and early adoption of emerging technologies also aids its market dominance.

What Are the Latest Trends in the Data Center Chip Market?

Changes in the data center chip market include the use of 5nm semiconductor processes to improve chip performance and energy efficiency. In addition, there is a trend toward integrating specialized hardware accelerators such as GPUs and TPUs to speed up AI and machine learning workloads. These developments are expected to eventually define the architecture of data centers and the future demand for advanced chip technologies.

Who Are the Key Players in the Data Center Chip Market?

Achronix Semiconductor Corporation, Advanced Micro Devices Inc., Arm Limited, Broadcom Inc., Fujitsu Limited, GlobalFoundries Inc., Huawei Technologies Co. Ltd., Intel Corporation, Marvell Technology Inc., Nvidia Corporation, Taiwan Semiconductor Manufacturing Company Limited. etc.

If you require any specific information that is not currently covered within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, considerations studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.